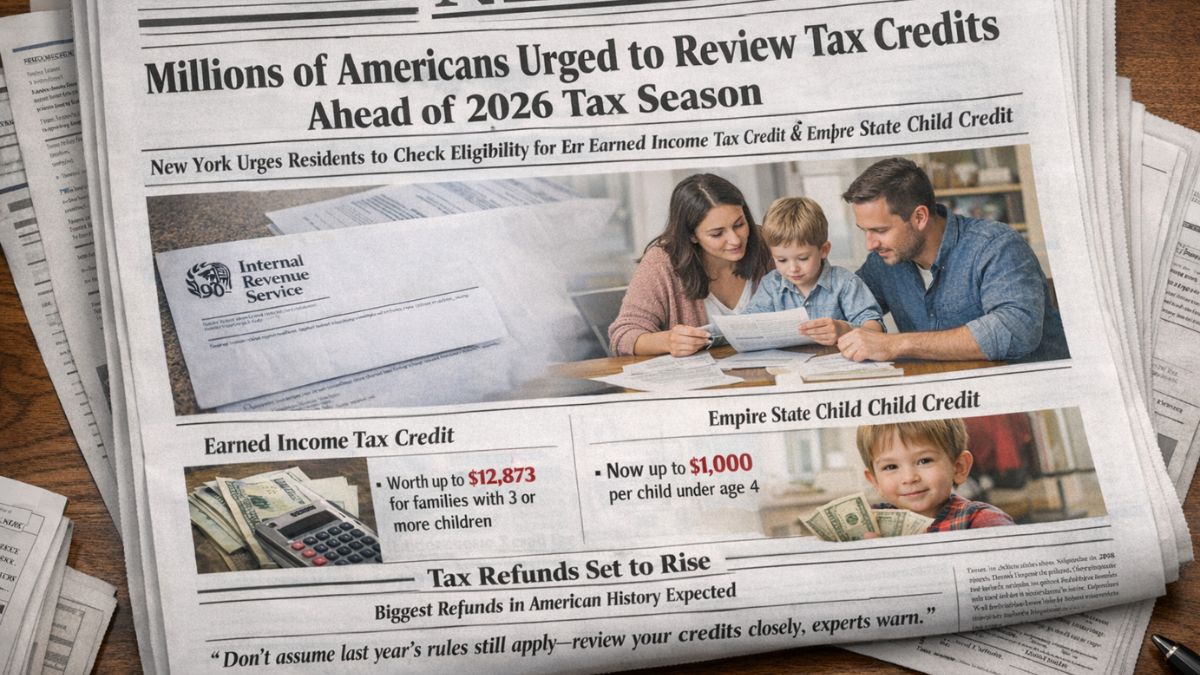

Millions of Americans Urged To Review Tax Credits – As the 2026 tax season draws closer, millions of Americans—particularly those living in New York—are being urged to take a fresh look at the tax credits they may be eligible for. With refunds expected to be higher than in previous years, reviewing eligibility could bring meaningful financial relief to working families who might otherwise leave money unclaimed.

New York State officials are placing special emphasis on two key credits for the 2025 tax year: the Earned Income Tax Credit and the expanded Empire State Child Credit. For many households, these programs could increase refunds by thousands of dollars.

Why This Matters Now

Tax season is already underway, and federal leaders have promoted what they describe as Working Families Tax Cuts. According to federal estimates, average refunds are expected to rise by roughly $1,000 per household, with more than 100 million households projected to receive some type of refund.

Families with children may benefit even more. Households with two children could see average tax cuts of around $1,700 due to enhancements in child-related credits. At a time when inflation continues to affect groceries, rent, childcare, and utilities, these refunds could provide much-needed breathing room.

New York State Urges Residents to Review Eligibility

The New York State Department of Taxation and Finance has encouraged taxpayers not to assume that last year’s tax situation still applies. State officials stress that many families qualify for credits without realizing it.

According to the department, both the Earned Income Tax Credit and the expanded Empire State Child Credit are designed to return real money to working households. The message is straightforward: failing to check eligibility could mean missing out on money you are legally entitled to receive.

Understanding the Earned Income Tax Credit

The Earned Income Tax Credit, commonly known as the EITC, supports low- to moderate-income workers. For the 2025 tax year, workers earning up to $68,675 may qualify, depending on household size and filing status.

One of the most important features of the EITC is that it is refundable. This means taxpayers can receive a refund even if they owe little or no federal income tax. When federal, state, and local EITC benefits are combined, families with three or more qualifying children could receive up to $12,873.

Expanded Empire State Child Credit Offers Bigger Support

The Empire State Child Credit has been significantly expanded this year. For children under age four, the maximum credit has increased from $330 to $1,000 per child. This expansion reflects rising costs related to early childhood care, food, and housing.

To qualify, taxpayers must be full-year New York State residents and have at least one qualifying child under the age of 17 by the end of the tax year. Like the EITC, this credit is refundable and can increase refunds even if no state tax is owed.

Credits vs. Deductions: A Key Difference

Financial experts emphasize that tax credits are far more powerful than deductions. A deduction reduces taxable income, while a credit directly reduces the tax bill dollar for dollar.

In practical terms, a $1,000 credit saves $1,000 in taxes, while a $1,000 deduction only saves a portion of that amount depending on income level. This distinction makes reviewing available credits especially important.

Don’t Rely on Last Year’s Rules

One common mistake is assuming eligibility stays the same each year. Income thresholds, credit amounts, and qualifying rules can change. Even small shifts in income, marital status, or number of dependents can affect eligibility.

Experts recommend reviewing both federal and state credits annually, even for taxpayers who have never qualified before.

Important Deadlines

Tax returns are due by April 15 unless an extension is filed. Filing early helps reduce errors and speeds up refunds, which can be critical for families relying on that money for essential expenses.

Final Takeaway

With larger refunds expected in 2026, many households may find extra financial relief if they take time to review their eligibility. Whether the money is used to pay down debt, build savings, or manage rising costs, the opportunity is significant. The key is simple: review the rules, file carefully, and don’t leave money on the table.

Disclaimer

This article is for informational purposes only and does not constitute tax or financial advice. Tax laws and eligibility rules may change. Always verify details with official sources or a qualified tax professional before filing.